New Homes Index: September 2022

‘September tries its best to have us forget summer’

Bernard Williams

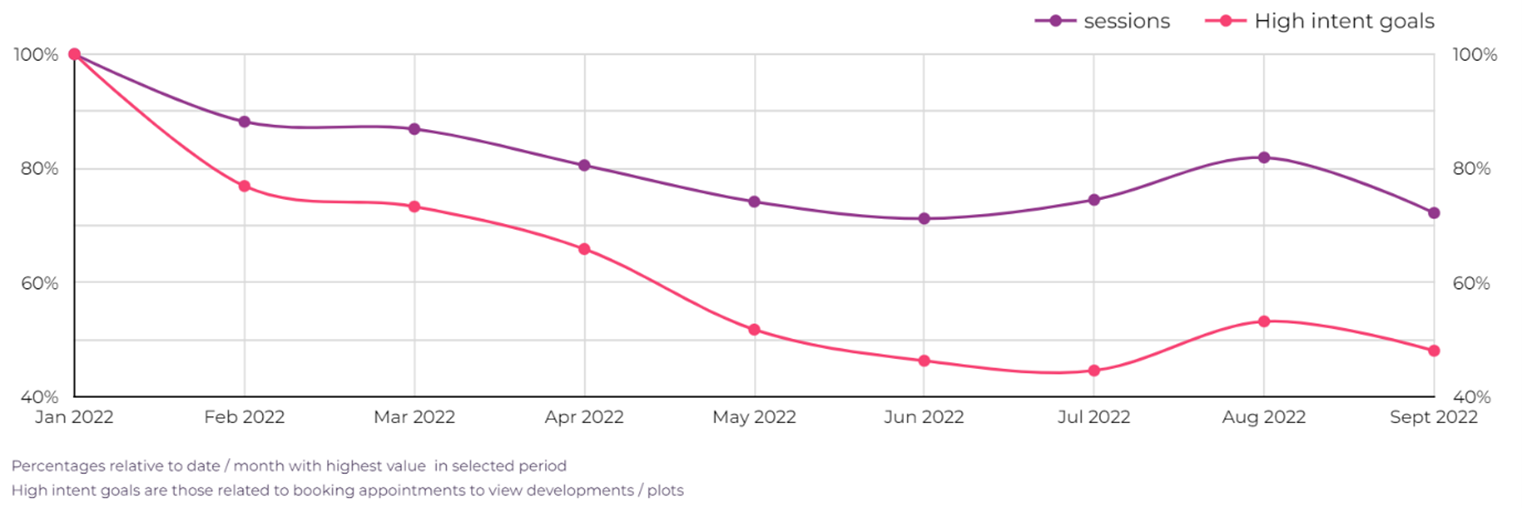

Monthly tracker

Of late, the first few days’ data on web traffic and high intent goals in any given month has proffered daily averages that can predict the performance of the ensuing weeks with a welcome degree of accuracy.

Unfortunately September didn’t quite provide us with that luxury. Initially pointing towards a relatively modest decrease in web sessions of -5% and a goals swing of -2.5% MoM, the headline figures ended up as -11.97% and -9.6% respectively.

In terms of web traffic to our developer pool, this MoM swing puts September on par with the same period in 2021, where an -11% drop in sessions MoM was an inevitable consequence of a sustained shortage of plots coupled with August ‘21 being the last chance to secure moves in England before the SDLT changed once again on 30th September.

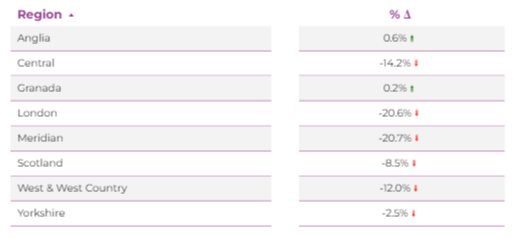

Total web session MOM change by region:

Daily tracker

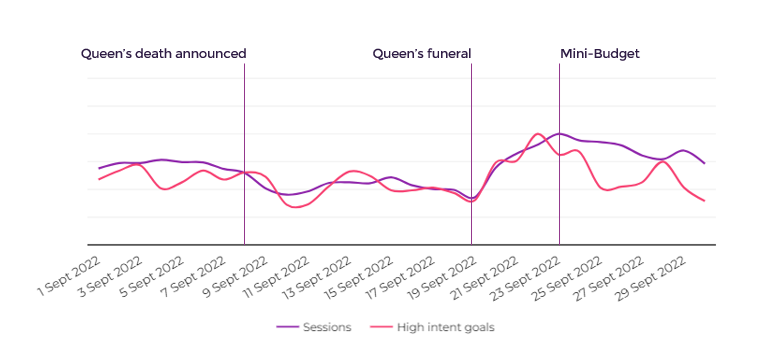

The many and varied events of the month ensure that viewing September as an homogenous whole is unhelpful to anybody in search of a governing narrative of the property market this autumn: this was a highly volatile period where consumer engagement reacted to the broader economic and cultural moment almost in real time.

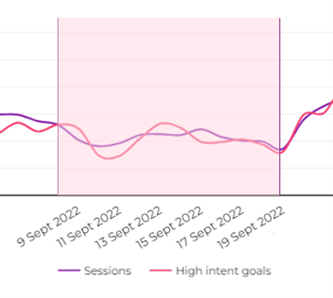

Reaction to the Queen’s death

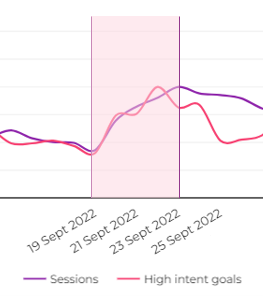

From the announcement of the Queen’s death (8th September) to the state funeral (19th September), web sessions (-29%) and high intent goals (-18%) plunged compared to the previous 12 days.

The consensus for respectfully suspending ad activity during this period impacted our dataset, with most developers pausing social and display on the Thursday and Friday up to and including the Monday of the funeral itself. For the most part paid search remained live, since the bulk of activity is surfaced only to those actively seeking properties and learning about brands.

Web sessions from organic sources were commensurate with paid channels, with a decrease over the same timeframe of -25%.

Ad activity restarts in earnest

As ad activity resumed in the immediate period following the funeral (20th-23rd September) web sessions increased to a peak index for the month on the 23rd; high intent goals index topped out on 22nd. Compared to daily averages recorded in the first week of the month, sessions were up +18% during this period and goals rose by just under a third.

With many budgets expressed monthly, this uptick in paid sessions was driven by an increase in daily expenditure following the period of inactivity. Organic traffic in this period increased +11% in comparison.

Hello tumultuous mini-Budget!

As previous reporting has showed, a stamp duty announcement will have immediate impact on the NHI. One of the historic peak months within our index coincided with the Spring Budget in March 2021, which delivered an extension to the stamp duty holiday laid out in the previous July as a post-Covid shot in the arm for the industry.

With September’s mini-Budget, web sessions remained at a buoyant level in the following week. This of course coincided with marketing output increasing following the state funeral: comparing the last ten days of September to the previous ten days, our property benchmark monitoring recorded just over double (that’s c.50,000,000 additional) the volume of ad impressions served across Google Ads, Meta and DV360 platforms.

As a result web sessions remained more or less unimpacted (-1%) by market or wider economic conditions for the remainder of the month, despite the furore that followed the non- budget. One attempt to unearth a coherent narrative might posit that increased interest engendered by the stamp duty changes and uncertainty caused by withdrawn mortgage products and spiking interest rates effectively cancelled each other out.

It’s clear however that increased daily expenditure with paid media also played a strong hand here in maintaining traffic levels to websites within our index: sessions from organic search decreased -14% in the same period.

Combined ad delivery index:

At the close of the month, high-intent goals returned to a daily average level more aligned to where September was in the first week before three weeks of significant national events. Whilst that isn’t immediately troubling, a drop of -29% in average daily goals compared to the pre-Budget / post-funeral period does represent a divergence from the consistent conversion rates of web sessions to those requesting appointments to view properties usually recorded over similar periods in the NHI. This likely reflects the growing share of traffic driven by paid media, which inevitably converts at a lesser rate than sessions from direct or organic sources.

**

For the same reason that it’s been particularly interesting for watchers of the market, September is of limited value as a bellwether for the coming months. For those looking to propound the idea of a resilient market that can carry on trading at pace, there’s evidence that might support that view; for anybody concerned that the rising cost of borrowing will choke off demand, there are already indications that this is the case. Ultimately of course, as September demonstrated, both things can be true: resilience can be engineered that will withstand a drop in demand or adverse market conditions, and a skilfully actuated marketing strategy, underpinned by robust interrogation of the available data will be central to that project.